Investment Commentary – Year in Review 2024 Greater Certainty of Uncertainty

Year in Review 2024 – Commentary

Although this is a year in review commentary, I will spend more time focusing on today and the future.

History is defined as a systematic study or documentation of our human past. We’ve all heard the expression history doesn’t repeat itself, but it rhymes. What I am more fascinated about is that today we are really living in historic times. I will give a number of examples about this and how it will affect all of our futures, especially from an investment perspective.

When we look at the investment landscape we see the second year of a bull market, which began at the beginning of 2023, after a short-lived bear market in 2022. 2024 came in like a lion and has actually gone out like a lion. Although the S&P 500 was up in excess of 25% for the second year in a row the market remained very thin with The Magnificent Seven- seven of the largest US technology companies- accounting for more than half of the gains. The past year saw the acceleration of artificial intelligence, which while not a new concept, was a major factor in boosting large cap technology stocks both in 2023 and 2024. Just this week history was made again as the emergence of DeepSeek, a new AI model out of China, has challenged the status quo of the Magnificent Seven and led to the largest ever single day market cap loss with Nvidia losing nearly $600 billion in value. Of course, the only question to ask now is: where do we go from here? As most of us know markets don’t go straight up forever.

Today there are many more risks than I have seen in over five decades in the investment industry. In this commentary I will highlight a few of them. The stock market is still in a honeymoon phase with President Donald Trump and yes, he has a meme coin called $TRUMP which has skyrocketed in value. In his first week in office he has performed more tasks and issued more executive orders than the last several presidents combined.

As he began serving his second non-consecutive term as President of the United States, let me share some facts about his first week in office. Starting on his very first day, he rescinded 78 executive orders given by President Biden. These included orders related to diversity, equity, and inclusion (DEI), opening the border and climate change, just to name a few. He then went on to sign his own 26 executive orders on his first day fulfilling a number of his campaign promises. Those included cracking down on immigration, energy, climate policies, and pardoning those who were found guilty in the January 6th riots. This is the man who said “he would not be a dictator, except for day one of his presidency”. For greater context, President Biden signed nine executive orders on his first day, Donald Trump signed one on his first day of his first presidency and Barack Obama and George Bush did not even sign one. I won’t get into politics and the American people have spoken, but with all of these changes and the speed with which they’re being made, it certainly makes me more nervous than I was a few weeks ago.

This all leads me to state many of the same issues that we’ve talked about in the past. The stock market is expensive based on a number of factors. Most compelling is the S&P 500 CAPE ratio dating all the way back to 1890. This metric is showing that US stocks are currently at an extreme valuation relative to their earnings, more than double their historical average.

S&P 500 CAPE Ratio

These high starting valuations along with the increasing list of geopolitical uncertainties and other risks have led major investment firms such as Goldman Sachs to predict annual US stock market returns of just 3% per year over the next 10 years as their base case.

Margin debt continues to be at an all-time high, where people have borrowed money to invest or gamble in the stock market. Technology has been driving the bus as a sector with the Magnificent Seven trading as if they can only ever continue to move up.

Then there is the risk of tariffs and every day in the newspaper we read about how they will affect, not just the Canadian economy, but Mexico, China and other global markets. We also know how inflationary it will be for the US economy.

Then there’s interest rates. The Fed started cutting rates on September 18, 2024, It’s first cut since March 2020. They started with a 50 basis point cut and since lowered their bank rate with two more cuts of 25 basis points for a total of one percent since September. Although short term rates are down 1%, the 10-year treasury is back up 1% almost to its previous high. This very much influences 30-year mortgage rates in United States, which are now above 7% once again. There is a great concern of re-inflation in America.

So where do we go from here? Our Family Office is the hub of a wheel in our client families’ lives. We are an extra set of eyes on their trusted advisors. We are their most trusted advisor as their Family Office. We simplify their lives and find solutions to their challenges which include, but are not limited to tax planning, estate planning, strategic philanthropy, risk management, education, tax preparation and bookkeeping.

Of course, we have a fiduciary responsibility to manage our clients’ investment liquidity. We’ve always done so by managing and focusing on risk. We are currently invested in 13 asset classes, which include 20 different strategies. We are very diversified and the risk we take is low relative to bonds and a small fraction of the risk of the stock market. We have an allocation to equities, but it is less than most because of the risk we currently see in equities. In the future, should the opportunity arise where we can find better returns in the market for a commensurate amount of risk, then we will be buying more stocks. In the meantime, we are looking at other asset classes that we expect to provide a much greater risk adjusted return than the stock market.

The most comforting attribute of investing in All-Weather Portfolios which are not dependent on public markets is that they perform in any market environment. However, they particularly shine at protecting capital in market crashes, as was proven when our All-Weather Portfolios were up in 2022 while a traditional 60% stock 40% bond portfolio was down -16%.

We are starting 2025 with stocks at extreme valuations and the most geopolitical uncertainty in recent history. There is no better time than the present to evaluate your own portfolio’s asset allocation and determine if your assets are adequately protected from today’s risks.

Year in Review 2024 – The Markets

The year of 2024 closed on an upbeat note, with stocks finishing the year on solid footing, but with plenty of volatility throughout the year, and significant dispersion across sector, geography, and individual names.

The S&P 500 index posted a 25% gain (in US dollar terms) for the year. This year’s rally was largely fueled by technology and AI stocks with the NASDAQ up 29.6%. The enthusiasm for generative AI and other innovations led to a significant concentration of market gains in a few mega-cap tech companies, pushing their valuation multiples higher. The so-called “Magnificent 7” – the 7 large-cap technology companies – contributed 55% of the return of S&P 500 index.

Additionally, post-election optimism contributed to gains, with markets responding favorably to expectations of tax cuts and regulatory easing anticipated during President Trump’s second term.

Despite the stellar annual performance, the year’s finish was more subdued. The final days of 2024 brought a bout of volatility across global stock markets, largely driven by a reset of expectations around U.S. monetary policy.

Unfortunately for stock market participants this volatility did not subside at the start of 2025. As mentioned earlier in this commentary, the unforeseen arrival of a competitive new AI model out of China has cast a shadow of doubt over some of the optimistic tech sector valuations.

As we reflect on the past two years of exceptional stock market performance, it’s important to keep a long-term perspective. Many investors still remember the pain from the double-digit percentage loss of their portfolios in 2022 – when The S&P 500 index lost 18%, and the Barclays Aggregate Bond index lost 13% in the same year. Looking at the past three years, The S&P 500 index returned an annualized 8.9%, close to its long-term average. For those who invest only in traditional stocks and bonds, the volatility during these years took investors through a roller coaster run.

Other equity markets such as Europe and Canada saw decent returns for the year, with 9% and 21% for the Euro Stoxx 600 and S&P/TSX Composite respectively (in local currency).

Inflation has steadily fallen over the past two years, which in turn has allowed central banks to start cutting rates. However, the last mile proved harder than markets anticipated. Many U.S. inflation measures remain close to 2.5%, rather than The Fed’s target of 2.0%. The US economy has remained fairly strong allowing the Fed to take rate cuts somewhat slower while watching the data. Other countries, such as Canada, are in a weaker economic position and have had to keep up the pace of rate cuts to avoid recession, causing a significant weakening of the CAD relative to the USD.

The U.S. Federal Reserve has repeatedly sounded notes of caution that the rate of disinflation appears to be slowing, and the inflation concerns may be back on the front burner.

In its December meeting, the Fed cut the policy rate by 25 basis points to 4.25% to 4.50%, as expected. The quarterly update of the Fed’s Summary of Economic Projections (SEP) revealed the median 2025 inflation forecast rising to 2.5% from the prior forecast of 2.1%.

The main surprise was in policymakers’ views on the appropriate pace of rate cuts next year, which was slashed in half and now shows only two 25-basis-point cuts for 2025. The shift in the expectation of future rate cuts captured investors’ attention and caused anxiety. Unusually, Treasury bond prices fell after mid-September, even as the Fed began cutting rates. Against this backdrop, U.S. Treasury bonds had a tough year, ending the year nearly flat.

Complicating matters, many investors fear that key policy measures favored by the incoming Trump administration – be it lower immigration which puts upwards pressure on labor costs, or the imposition of tariffs which puts upwards pressure on goods costs – will lead to inflation remaining stubbornly high.

This possibility of inflation resurgence has in turn anchored longer-term interest rates. In the fourth quarter of 2024 the U.S. 10-year bond yield rose significantly from 3.8% to 4.6%, despite the Fed’s cutting of short-term rates. The rise in the 10-year yield reflects the market participants’ concerns of inflation in the future.

Looking ahead to 2025, investors should question whether the same drivers of performance will remain in play. We keep a close watch on the risks and note all the key ingredients to trigger a correction are in place: overly concentrated stock market, a recent run of outsized returns, and rising competition for investment dollars from bonds.

There have been 40 corrections of 10% or more in the S&P 500 since 1950, or one roughly every couple of years. Minimizing this volatility as much as is practical is a key objective of our investment philosophy. In fact, seeking to minimize this volatility while still striving for sustained capital appreciation is what we think makes our approach unique.

Year in Review 2024 – Charts

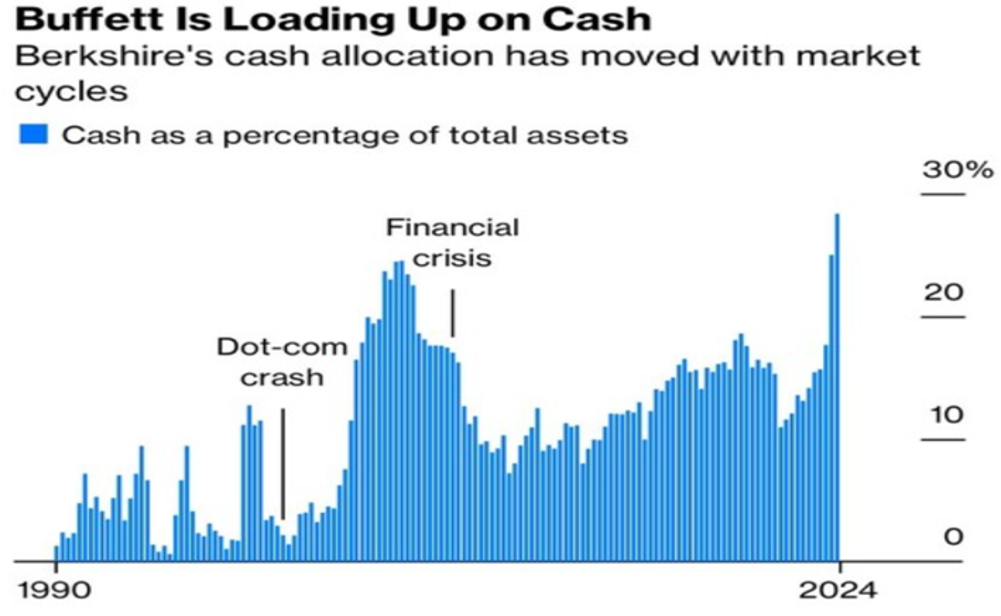

- The above chart shows Berkshire Hathaway’s cash position as a % of its total portfolio assets

- Historically Buffett has made significant increases in his cash position before, notably prior to the Dot-Com Crash and The Great Financial Crisis

- The chart shows that recently Buffett has increased his cash position to a historic high of nearly 30%

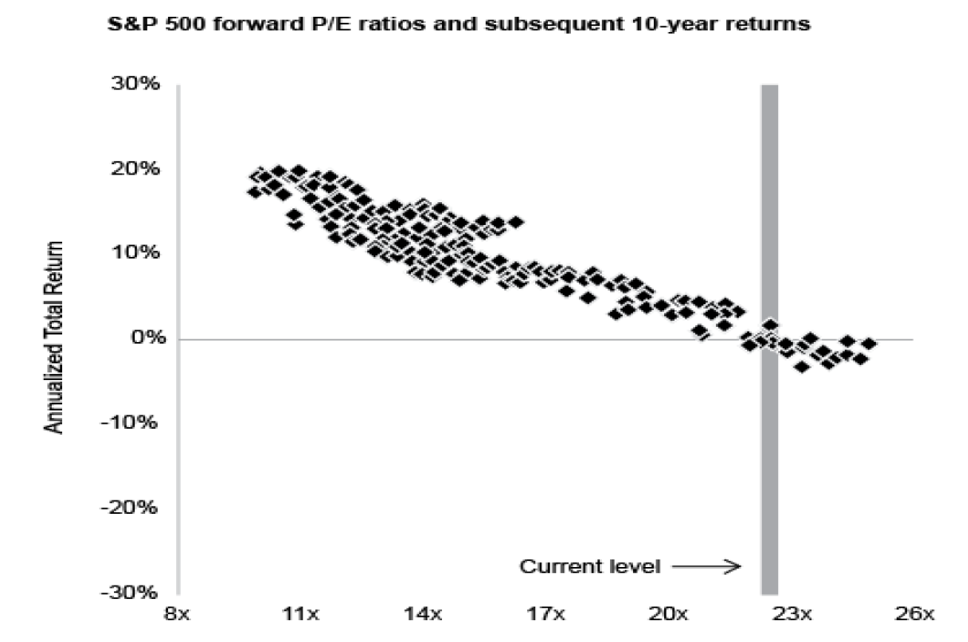

- The above chart shows the forward price to earnings ratio (x-axis) and subsequently what the annual returns were over the next 10 years (y-axis) for the S&P 500

- There is a clear trend that higher starting valuations result in lower returns over the next 10-year period

- Historically, when valuations are at levels we are currently seeing (highlighted grey) the returns for the S&P over the next 10 years have ranged between +2% and -2% per year.

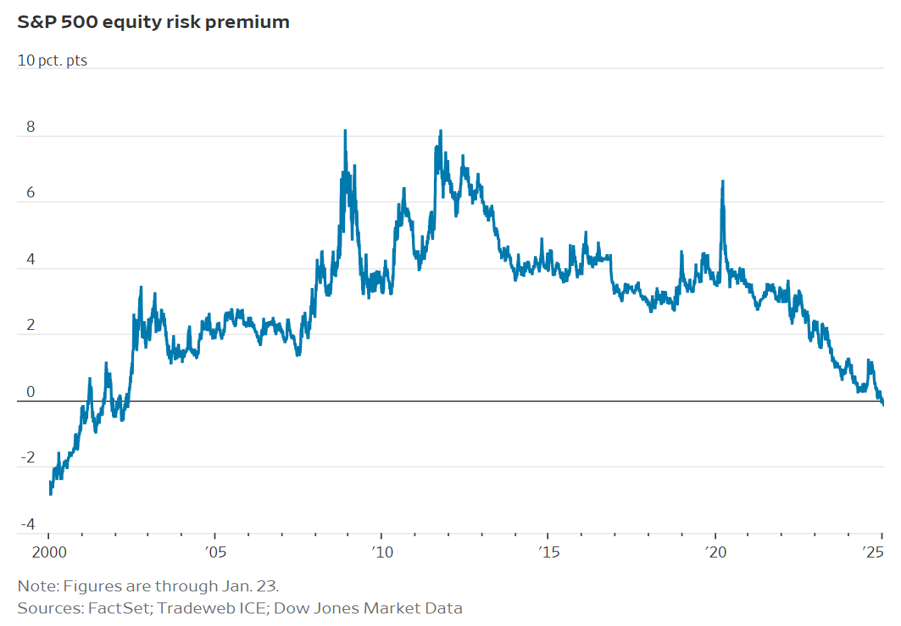

- The equity risk premium shows the difference between the earnings yield on the S&P 500 and the yield on 10-year Treasurys

- The difference between the earnings yield on risky stocks and the interest yield on relatively riskless government bonds shows how much investors are being compensated for taking on the extra risk of owning stocks over bonds

- In December of 2024 the equity risk premium turned negative for the first time since 2002, meaning at current valuations investors are not being compensated for the additional risk of owning US stocks

Download a copy of this article in pdf here.

Insights

View AllNews & Events

News & Events

Keep up to date on Our Family Office's latest firm news, events, global and regional awards, as well as the latest announcements.

Tim Cestnick’s Globe & Mail Articles

Tim Cestnick's Globe & Mail Articles

Catch up on our Co-Founder and CEO, Tim Cestnick's weekly column. His status as an expert is reinforced by his role as a tax and personal finance columnist for The Globe and Mail, Canada’s most prominent national newspaper.

Investment Thinking

Investment Management

We provide tax-efficient preservation and growth of your investment assets, utilizing best-in-class global strategies, strategic asset allocation, rigorous due diligence on managers and their selection.

Podcasts

Podcasts

Our Family Office proudly presents the Our Family Office Podcast. Throughout the inaugural season, host Adam Fisch speaks to various experts from across our firm, offering insights into the areas of focus for an integrated family office, and the ways that a Shared Family Office™ can help Canada’s wealthiest families.