Investment Commentary – Q1 2026 When Chaos Surrounds You

Q1 2026 – Commentary

I am writing this after returning from a two-day conference in New York. The first day focused on Fintech, while the second centered on investments. Notably, 95% of the Fintech discussions revolved around artificial intelligence, with the majority of dialogue highlighting its positive aspects. It was only by mid-afternoon that I raised a question concerning the potential downside risks of AI, particularly following discussions on the dark web and cybersecurity. While artificial intelligence is indeed transformational, it is important to acknowledge that its impact is not exclusively positive.

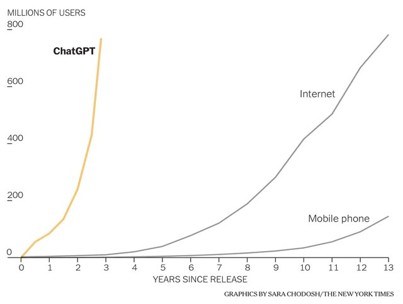

I challenged the panel to consider the possible displacement of tens of millions of workers due to AI adoption, as well as the broader implications for the global economy and geopolitics. Although responses were far-reaching and speculative, since no one can predict the future with certainty, the rapid uptake of tools like ChatGPT and Copilot has been remarkable. Many experts compare the transformative nature of AI to that of the personal computer, the Internet, and mobile phones, asserting that AI will have an even greater effect on our daily lives.

Most presentations emphasized productivity improvements and suggested that many roles currently held by humans could eventually be replaced by humanoid technologies. However, until recently, there has been limited discussion regarding the potential negative consequences.

Nobody can say for certain which of these drawbacks will materialize or the extent of harm they may cause. Some concerns relate directly to the use of AI, for instance: how it will increase the effectiveness of cyber attacks? Recently the major AI firm Anthropic delayed the release of its latest model (Mythos) specifically due to these security concerns. Others worry of the second order impacts: what if increased automation outpaces the creation of new jobs? Some of the more cynical projections suppose a spike in unemployment to near 20% which would be worse than during the Great Financial Crisis and on a similar scale to The Great Depression era of the 1930’s.

A common theme in today’s market seems to be a tunnel vision on the positives along with a willful ignorance of the risks. This psychology is present not only in the area of AI but across the investment landscape.

Take the recent war with Iran as another example. After a brief bout of volatility in the markets coinciding with the start of the conflict, every positive headline mentioning the potential for peace talks or opening the Strait of Hormuz has resulted in stocks climbing to new highs. Any timeline on a real resolution is still uncertain yet the market is already pricing in a positive outcome. Even if the hostilities came to an end today, what are the risks of the damage that has already been done? It is estimated that up to $58 billion worth of energy infrastructure has been damaged including 30-40% of Gulf refining capacity which could take up to three years to repair. The price of energy will have a meaningful impact on inflation going forward and disrupted supply, either from a blockade (which may or may not be resolved quickly), or from reduced refining capacity (for which there is no quick fix) is not a positive in this regard.

Another area where we see the downside of risk being discounted is in the use of leverage. We see it with governments taking on historic levels of debt and we see it with investors who are borrowing to invest. Through the bull market these investors have likely seen the benefits of amplified returns but when eventually faced with a significant drawdown they will have to face the reality of margin calls, forced selling and magnified losses.

Leverage does not discriminate and can be devastating even for the most astute investors. One such investor was a man named Rick Guerin, the third member of an investment trio with Warren Buffet and Charlie Munger. Buffet even proclaimed that Geurin was just as smart as himself and Munger, the defining difference was that he was in a hurry to get wealthy and used leverage to amplify his returns. The result was that in the stock market downturn of the early 70’s Rick faced margin calls and was forced to sell his Berkshire shares at roughly $40 each. For context, those shares now trade above $700,000 each and that forced sale is estimated to have cost him over $10 billion by the time of his death in 2020.

In investing, opportunity and risk go hand in hand and we strongly believe you must always keep both in focus. Having an eye only for opportunity while neglecting the associated risks, whether that be in the context of AI, elevated valuations, the use of leverage or any other area of investment, can have devastating consequences. At Our Family Office we spend much of our time analyzing what can go wrong, so we can be prepared to manage our clients’ assets whatever the future brings. Our emphasis on risk and capital protection has served us well in past market corrections and with continued careful oversight we expect it will continue to serve us well in the future.

Q1 2026 – The Markets

The first quarter of 2026 marked a sharp shift in financial market dynamics. The year started favourably with the support of solid economic fundamentals. The market reached a record high by mid-January, as investors anticipated continued earnings growth across multiple sectors. A late February escalation of geopolitical conflict in the Middle East triggered considerable market volatility and investor concerns, overwhelming the early year narrative of gradual monetary easing and moderating inflation.

Following US and Israeli strikes on Iran a blockade of the Strait of Hormuz caused a sharp energy shock as roughly 20% of global oil supply transits through this important maritime chokepoint. Brent crude rose approximately 70% over the quarter, while WTI breached US $100 per barrel for the first time since 2022. The surge in oil prices re-ignited inflation concerns, drove a global sell off in risk assets, forced a rapid repricing of interest rate expectations across developed markets, and created considerable uncertainty for the global economy and financial markets.

US equities experienced significant volatility and the S&P 500 Index fell 4.3% (in US dollar) during the first quarter. That marked the weakest quarter for US large cap equities since 2022. Energy was unsurprisingly the top performing sector for the quarter (+38%) while the consumer discretionary, information technology, financial and health care sectors all ended the quarter with negative returns.

For reasons apart from geopolitics, Information Technology stocks declined during the quarter. The Nasdaq 100 Index fell 6% (in U.S. dollar), reflecting sensitivity to higher yields and valuation compression in growth stocks. The software sector was particularly hard hit. The evolving AI narrative has created a dichotomy within technology. Investors rotated towards AI infrastructure businesses such as semiconductors, cloud computing and data-centre providers, and away from traditional software stocks over concerns that generative AI could undermine the software-as-a-service subscription model the industry has relied on for years.

Canadian equities held up better. The S&P/TSX index stayed positive for the first quarter at +3.94% (CAD). The index’s heavy weighting toward resources worked in its favour, with energy stocks benefiting from the jump in crude prices.

European equities declined in Q1, with the MSCI Europe ex UK Index returning -2.2% (EUR) due to energy price sensitivity amid heightened geopolitical risk.

Emerging market equities were relatively resilient in Q1 2026. The MSCI Emerging Markets Index returned +0.2% (USD), outperforming developed markets amid commodity strength and regional dispersion (e.g., large technology-oriented markets of Korea and Taiwan outperformed).

In March, the war in the Middle East dominated markets, introducing volatility and a significant sell-off in government bonds. While there was some regional divergence, government bond yields rose across the board (yields move inversely with prices).

US Treasuries proved most resilient to the events of the quarter, while yields rose more sharply in other major markets. In Q1 2026, the US Aggregate Bond Index experienced largely flat performance, with a return of -0.05% for the quarter. U.S. mortgage, Treasury and agency bonds performed well this quarter, while high-yield and emerging market bonds lagged in the first quarter amid risk-off sentiment.

At its March meeting, the Federal Reserve (Fed) held rates steady at the 3.5%–3.75% range, and continued to signal one rate cut this year, citing persistent inflation and economic uncertainty stemming from the conflict in Iran. By then, markets had largely priced policy rates to remain restrictive for longer.

The Bank of Canada maintained a cautious stance, holding rates steady as well in its March meeting, citing renewed upside risks to inflation from higher energy prices and trade related uncertainty. Policy remained restrictive, with forward guidance emphasizing data dependence rather than easing. The Bank of Canada projected 2026 GDP growth of ~1.1%, constrained by trade disruptions and weak external demand.

Yields of Canadian benchmark bonds rose 50+ basis points, and the shorter-end experienced sharper increases. They’ve since stabilized and come off their peaks. Canadian bonds, as a whole, earned a positive return of +0.29% for the first quarter, as both the increase to yields and to spreads were modest enough that the bonds’ coupon payments more than offset them.

Despite recent themes of de-dollarization the US dollar appreciated against most major currencies in Q1, reflecting safe haven flows and relatively stronger US growth. This is in line with historical precedent as the US dollar typically appreciates during periods of global market volatility. The Canadian dollar slipped 2.1% against the U.S. dollar, a somewhat counterintuitive move given the surge in oil prices, which would normally support the Canadian dollar. This time, however, the sheer scale of global capital flowing into the U.S. dollar overwhelmed the domestic tailwind from energy.

The first quarter illustrated that despite a backdrop of market optimism traditional portfolios of stocks and bonds are still vulnerable to geopolitical turmoil and inflation shocks. This reinforces the importance of diversification into strategies that provide protection against inflation, stock market volatility and potentially higher interest rates. At Our Family Office we constantly evaluate these types of non-traditional strategies to build All-Weather Portfolios that are fortified against whatever uncertainty we may face in the future.

Q1 2026 – Charts

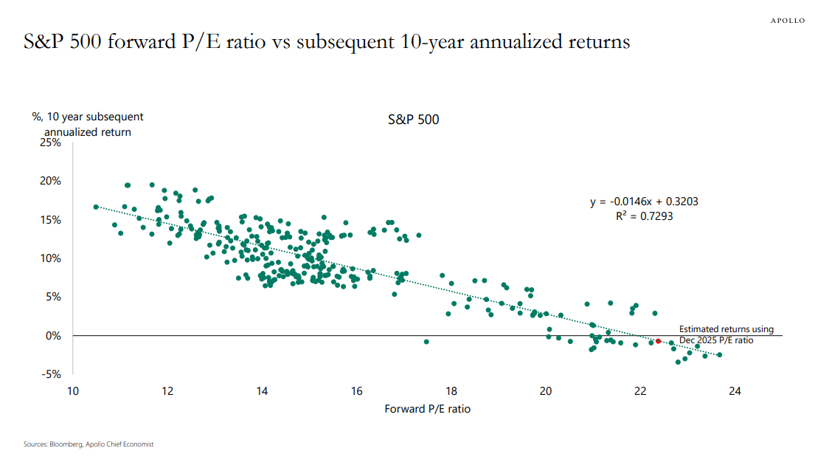

- The above chart shows the forward price to earnings ratio (horizontal axis) and subsequent annualized returns over the next 10 years (vertical axis) for the S&P 500.

- There is a clear trend that higher starting valuations result in lower returns over the next 10-year period.

- When valuations are at the levels we are currently seeing (the red dot on the chart), the historical trend implies negative annualized returns over the next ten years.

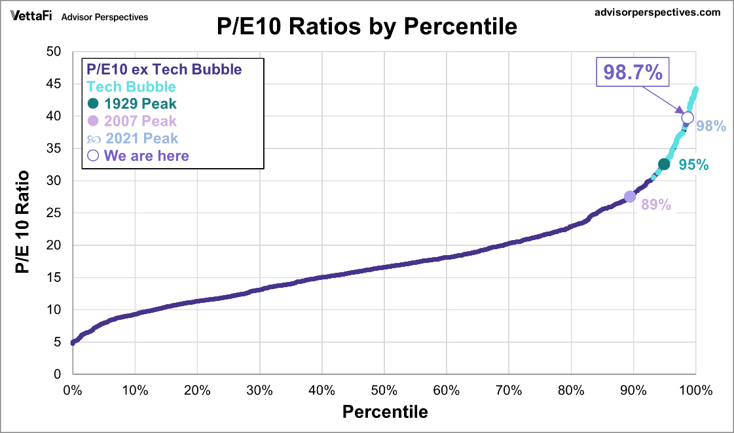

- The P/E 10 Ratio was developed by Benjamin Graham and David Dodd to devise a more accurate way to look at market valuation.

- This indicator looks at 10-year average earnings relative to the current price of the index, which smooths out temporary extreme valuation fluctuations.

- The above chart shows that the current P/E valuation of the S&P 500 sits at the 98.7% percentile, a historically very elevated level higher than 1929 and 2007 and in the same valuation range as the Tech Bubble.

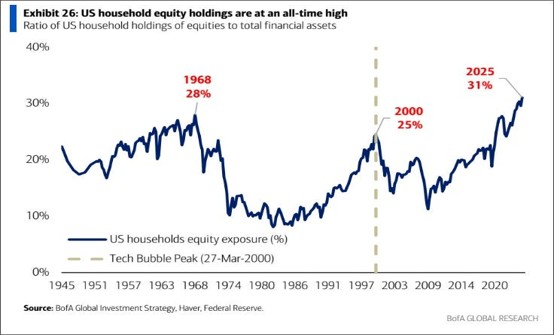

- The above chart shows what percentage of US households’ financial assets are in the stock market.

- Previous times where this metric peaked were prior to the bear market of 1968 and prior to the Dot-Com crash in 2000.

- The current reading of 31% is higher than all previous peaks since 1945, reflecting a historic high in stock market exposure for US households.

Download a copy of this article in pdf here.

Insights

View AllNews & Events

News & Events

Keep up to date on Our Family Office's latest firm news, events, global and regional awards, as well as the latest announcements.

Tim Cestnick’s Globe & Mail Articles

Tim Cestnick's Globe & Mail Articles

Catch up on our Co-Founder and CEO, Tim Cestnick's weekly column. His status as an expert is reinforced by his role as a tax and personal finance columnist for The Globe and Mail, Canada’s most prominent national newspaper.

Investment Thinking

Investment Management

We provide tax-efficient preservation and growth of your investment assets, utilizing best-in-class global strategies, strategic asset allocation, rigorous due diligence on managers and their selection.

Podcasts

Podcasts

Our Family Office proudly presents the Our Family Office Podcast. Throughout the inaugural season, host Adam Fisch speaks to various experts from across our firm, offering insights into the areas of focus for an integrated family office, and the ways that a Shared Family Office™ can help Canada’s wealthiest families.