Q1 2022 Investment Commentary

Q1 2022 – The Markets

The first quarter provided investors with a painful reminder that markets can turn volatile for any number of reasons. Multiple factors drove negative returns in Q1, from Russia’s invasion of Ukraine to the Fed’s increasingly hawkish response to elevated inflation. The interconnected nature of today’s world means the impacts of these shocks are not limited to the geographies where they occur but reverberate through global economy.

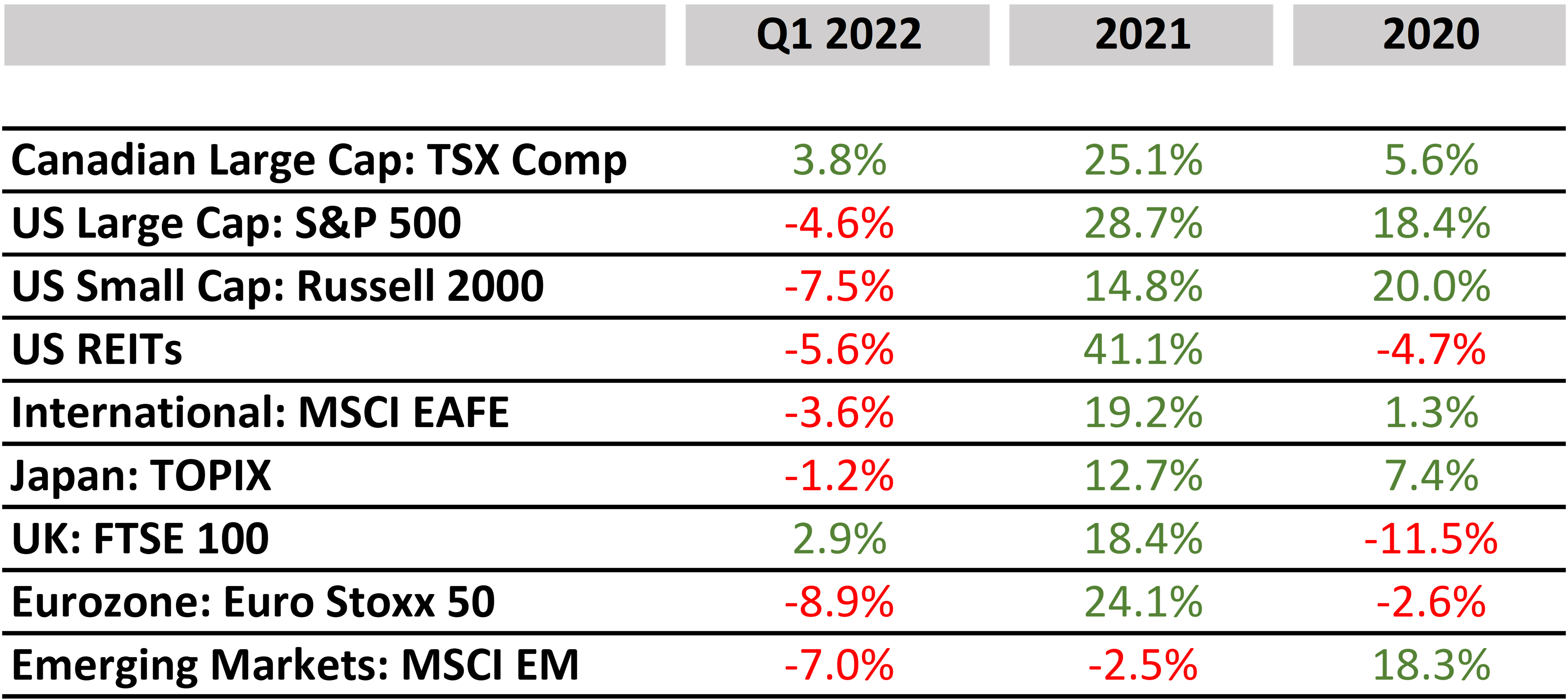

The general theme for equity markets was negative for the quarter but there were select markets that, owing to their weightings in certain sectors, produced positive returns.

The US market was not spared, printing negative returns in January and February, even a bounce back in March could only bring the S&P 500 back to -4.6% for the quarter. Within the market there were some noteworthy differences in performance: large caps outperformed small caps and value stocks outperformed growth stocks. Although some economic indicators were positive (unemployment continuing to decrease) increasing interest rates and the war in Ukraine were headwinds that could not be overcome.

Conversely, the Canadian market was one of the few that produced a positive return for the quarter. The S&P/TSX Composite, benefitting from a relatively heavy weighting to the commodity sector, gained +3.8% in Q1.

Energy and materials were the largest contributors to performance by a significant margin. Those sectors also happen to be the second and third heaviest weightings in the index (after financials).

It is no surprise that European markets, given their proximity to the situation in Ukraine (both geographically and with respect to economic ties), suffered disproportionately. The MSCI Europe index was down -7.2% as reliance on Russian energy and increasing supply chain disruptions proved to be major issues.

The emerging markets also had a difficult quarter with the MSCI Emerging Market Index down -7.0%. Representing a diverse group of countries and sector exposures, performance within the index was a mixed bag. Markets with significant commodity exposure (Brazil, Kuwait, UAE, Saudi Arabia, South Africa) performed well. However, the main driver of performance with a weighting of over 30% was China at -14.2%. In addition to dealing with the previously mentioned global growth headwinds China also instituted new COVID lockdowns in some major cities including Shanghai.

Energy and materials were the largest contributors to performance by a significant margin. Those sectors also happen to be the second and third heaviest weightings in the index (after financials).

It is no surprise that European markets, given their proximity to the situation in Ukraine (both geographically and with respect to economic ties), suffered disproportionately. The MSCI Europe index was down -7.2% as reliance on Russian energy and increasing supply chain disruptions proved to be major issues.

The emerging markets also had a difficult quarter with the MSCI Emerging Market Index down -7.0%. Representing a diverse group of countries and sector exposures, performance within the index was a mixed bag. Markets with significant commodity exposure (Brazil, Kuwait, UAE, Saudi Arabia, South Africa) performed well. However, the main driver of performance with a weighting of over 30% was China at -14.2%. In addition to dealing with the previously mentioned global growth headwinds China also instituted new COVID lockdowns in some major cities including Shanghai.

Q1 2022 – Interest Rates and Inflation

The fixed income markets likely did not live up to the expectations of traditional investors who count on their bond allocations to balance out the equity risk in their portfolios. When stock markets are down traditional investors hope that the conservative bond portion of the portfolio will act as ballast. Clearly that was not the case this quarter.

Persistent inflation and the response by central banks of raising interest rates was the key factor driving bond performance for Q1. In March year over year inflation hit 8.5% in the US (a four-decade high) and 6.7% in Canada (the largest increase since January 1991). An increase in consumer demand coming out of COVID, supply chain issues and rocketing energy prices were the main push factors.

The conflict in Ukraine has also exacerbated these issues. There are the obvious supply side impacts of curbing Russian oil imports and other sanctions. There are also less obvious contributors – Ukraine is responsible for producing approximately half of the world’s semiconductor-grade neon (used to produce semiconductor chips). Both Russia and Ukraine are not only large exporters of grain and wheat, but also of fertilizer which other countries rely on to maintain the yield of their crops. The conflict created additional supply chain issues just as some of the COVID related impacts were improving.

Inflation is here and the central banks have taken note by increasing rates and signalling a more hawkish policy and quicker rate hikes in the future. Both The Fed and the Bank of Canada increased rates by 25 basis points in March to 0.5%.

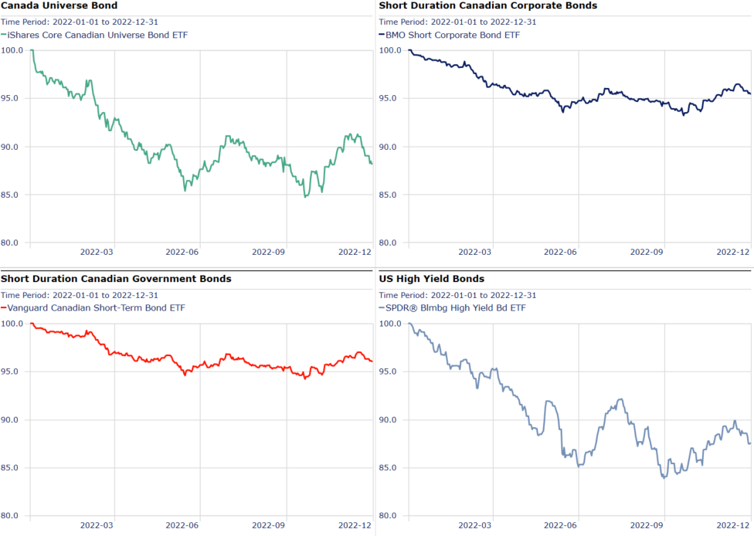

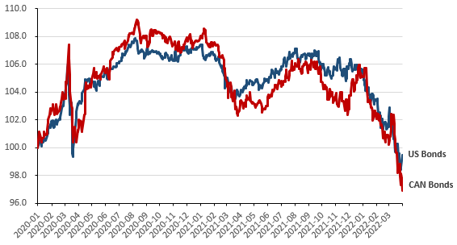

Bond markets felt the pressure of increasing rates with the US 10-year Treasury yield rising to 2.3% (up 81 basis points) the Bloomberg US Aggregate Bond Index was down -5.9% and the Bloomberg Canada Aggregate Bond Index down -6.8%.

The primary factor in how these rate increases impact fixed income is known as duration. The duration of a bond (or portfolio of bonds) measures the price sensitivity to changes in interest rates. In general, bond prices move inversely to interest rates. Put simply – if interest rates go up, bond prices go down and vice versa. A higher duration portfolio of fixed income will be more negatively impacted by increasing rates than a lower duration portfolio all else being equal.

This is one important lever investors can pull to protect their portfolios given the current environment of hawkish central banks and rising interest rates. Reducing the duration of your portfolio can have dual benefits. Firstly, your investments, being lower duration, will be less sensitive to the movement in interest rates (i.e. they will go down less in price if rates continue to rise). Secondly, shorter duration means that fixed income investments will come to the end of their term sooner, and when that principle is repaid it can be re-invested at the new higher rates.

Q1 2022 – Final Thoughts

The makeup of bond and equity allocations in a portfolio are surely important, from diversification to managing duration risk. However, the most important factor in determining returns is not any adjustment that can be made within an asset class but rather the overarching asset allocation as a whole. To weather periods where both of the traditional asset classes fall in tandem, just as the equity and bond markets did in the first quarter, Non-Traditional asset classes must be incorporated.

At Our Family Office our portfolios are much lower in both traditional equity weightings and duration of fixed income. This is possible because we are able to select investments from a much wider opportunity set and build meaningful allocations to Non-Traditional asset classes. Many of these investments are absolute return strategies which produce positive returns even in conditions where markets are down significantly. The inclusion of these strategies, which are far less correlated to public markets, allows All Weather Portfolios to protect client capital and achieve superior risk adjusted returns beyond what can be achieved with traditional solutions.

Q4 2022 – Market Snapshot

Performance Snapshot: Equity Markets

Performance Snapshot: Fixed Income Markets

Performance Snapshot: Updated Selected Market Returns

Financial markets saw respite in the final quarter of 2022 as decelerating inflation data aided market sentiment even as the Fed’s tone remained largely hawkish.

Despite a difficult December global equities posted strong quarterly numbers. However, after a volatile year for the markets, the fourth quarter rebound was not enough to bring 2022 returns into positive territory. Standout sectors in Q4 for the S&P 500 were energy (+22.83%), industrials (+19.21%,) and materials (+15.03%) with consumer discretionary (-9.09%) being the biggest laggard for the quarter. In the Canadian market the energy (+12.87%) and technology (+11.21%) sectors posted the biggest gains, with health care lagging (-11.32%).

Emerging market equities followed their developed counterparts in posting a quarterly gain. The emerging markets were aided by a weaker US dollar and positive sentiment in China stemming from a relaxation of its zero-COVID policies.

Central banks continued on their path of rate increases to bring inflation in line. The Fed raised rates twice in Q4 to end the year at 4.50%. Similarly, The Bank of Canada increased rates twice bringing its target rate to 4.25%. Even as Central Banks continued to hike the fixed income markets rallied to end the year. It seems that in Q4 Investors had already priced in the widely expected higher rates. Both policy makers and investors will be keeping a close eye on inflation in 2023 as a key driver of future interest rate decisions.

Q1 – 2022 – Charts

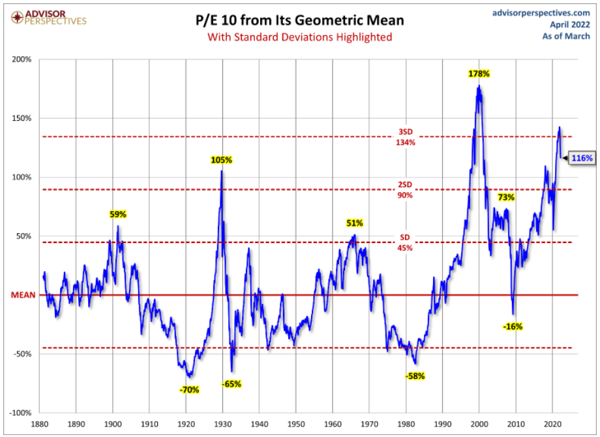

- The P/E 10 ratio divides the price of the S&P500 by a 10-year average of inflation-adjusted earnings, effectively smoothing out fluctuations in the business cycle.

- This 140-year graph showing the Price Earnings (P/E) Ratio with risk being highlighted, shows that the market is currently priced second only to that of the Tech Bubble (2000).

- When the ratio exceeds 2 standard deviations above the mean, as it currently is, bear markets have historically followed. Unless earnings catch up to close the gap, this should be seen as unsustainable.

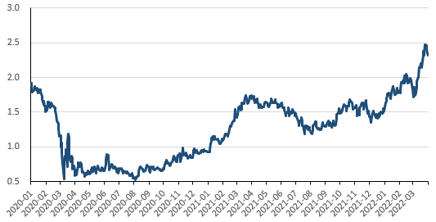

Chart 1: Ten Year U.S. Treasury Yield (%)

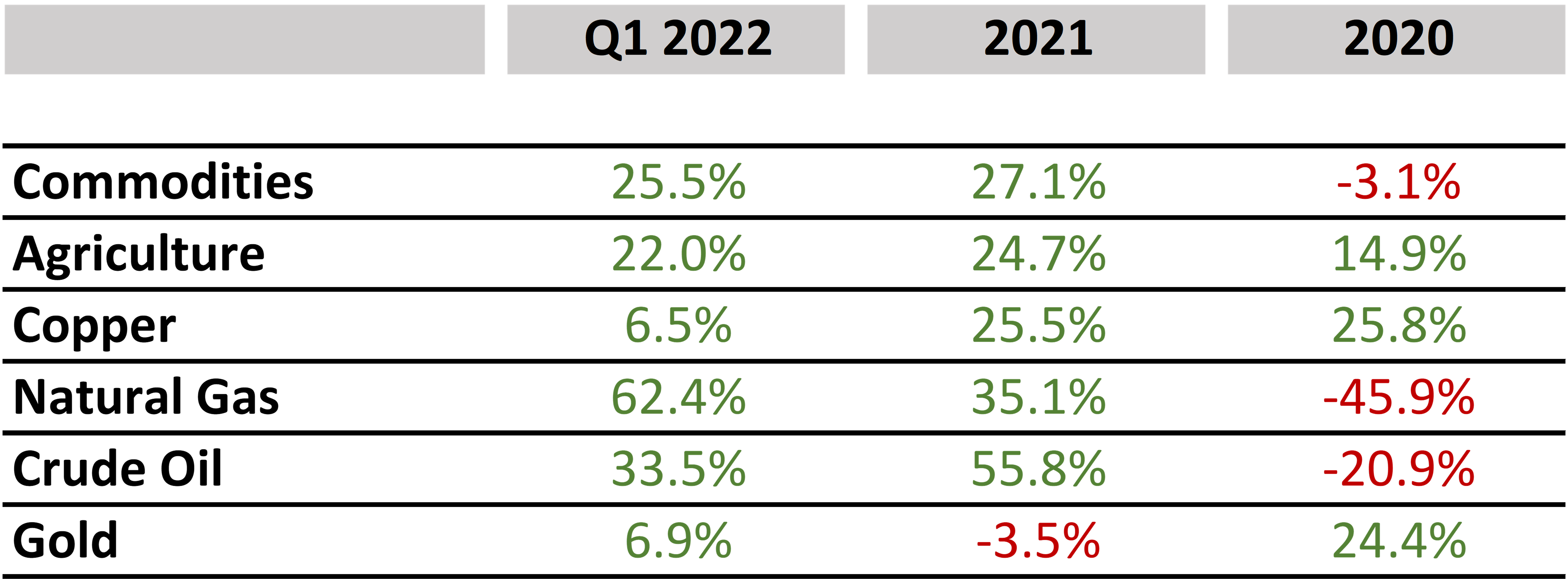

Table 1: Commodities (USD)

Chart 2: Canadian & U.S. Bond Market Performance

Table 2: Summary of Global Equity Returns

Download a copy of this article in pdf here.

Insights

View AllNews & Events

News & Events

Keep up to date on Our Family Office's latest firm news, events, global and regional awards, as well as the latest announcements.

Tim Cestnick’s Globe & Mail Articles

Tim Cestnick's Globe & Mail Articles

Catch up on our Co-Founder and CEO, Tim Cestnick's weekly column. His status as an expert is reinforced by his role as a tax and personal finance columnist for The Globe and Mail, Canada’s most prominent national newspaper.

Investment Thinking

Investment Management

We provide tax-efficient preservation and growth of your investment assets, utilizing best-in-class global strategies, strategic asset allocation, rigorous due diligence on managers and their selection.

Podcasts

Podcasts

Our Family Office proudly presents the Our Family Office Podcast. Throughout the inaugural season, host Adam Fisch speaks to various experts from across our firm, offering insights into the areas of focus for an integrated family office, and the ways that a Shared Family Office™ can help Canada’s wealthiest families.