Investment Commentary – Year in Review 2025 : How High Is Up? What We Know and What We Don’t.

Year in Review 2025 – Commentary

We often joke on the investment team at Our Family Office that our clients have simple but demanding expectations: when markets are up, they expect to be up and when markets are down, they still expect to be up. Since inception, we have met those expectations through disciplined strategic asset allocation.

At the heart of our approach is a focus on risk. The ultra-high-net-worth families we serve share this philosophy. While it can feel uncomfortable not chasing the herd, we are confident in our process. Markets don’t go straight up forever, and our job is to look for opportunities that offer attractive returns with minimal risk.

It would be an understatement to say we live in volatile times. Hardly a week goes by without a global event that makes us stop and ask, “Did that really just happen and what does it mean for the future?” Especially in the United States, we are witnessing an extraordinary number of “firsts,” and how history ultimately judges them remains to be seen.

Financial markets remain exuberant. Asset bubbles continue to inflate, and double-digit returns have not been limited to equities alone. Commodities such as gold, silver, and copper, along with Bitcoin, also reached new highs in 2025.

Against this backdrop, a key question looms: are we experiencing rational exuberance driven by the mega-trend of artificial intelligence, or is it something more dangerous?

Only time will tell. What we do know is that every investment ultimately comes down to return on invested capital (ROIC): what kind of profit is an investment generating from the capital invested in it? While AI is undoubtedly a game changer, the scale of spending, trillions of dollars on infrastructure, raises an important question: what returns are companies expecting? If those returns fail to materialize, stock prices could fall sharply and potentially drag the broader market down with them.

Fear of missing out is nothing new. We saw it in 2025, just as we did during the subprime mortgage crisis in 2008, the dot-com bubble in 2000, The Nifty crash in the early 70s, the crash of 1929, the Mississippi Company land scheme, and even Tulip mania in 17th-century Holland. Bubbles inflate, some more than others, and they eventually burst. No one, including us, knows when that will happen, but history teaches us that asset prices do not rise forever. Recent corrections in markets like the Toronto condo market are a timely reminder.

The year 2025 was exceptional in terms of surprises. President Trump’s tough rhetoric and tariff actions, referred to as “Liberation Day”, introduced new volatility. Interest rates stayed higher for longer, geopolitical conflicts escalated, and the so-called “Magnificent Seven” stocks were, at times, less than magnificent. Investors began dialing back risk and rotating toward more value-oriented opportunities.

It was also a year of political surprises closer to home. Canada elected a new Prime Minister, and remarks about Canada potentially becoming the 51st U.S. state added another layer of uncertainty, hardly helpful as CUSMA trade negotiations approach in 2026. We are living through a period of history that few could have predicted, and while opinions on leadership and policy may differ, it is difficult to argue that the world feels safer today.

In this environment, our role as stewards of capital is clear. Our Family Office is a Shared Family Office®, and one of our core responsibilities is managing client liquidity. We are asset allocators by design. Rather than focusing solely on stocks and bonds, we allocate across 13 different asset classes, working with 18 global managers and 21 distinct strategies.

Our goal is simple: achieve good returns with very low risk. Our portfolios are built to weather storms, and historically, when markets have gone down, our portfolios have held up remarkably well.

Our clients are already wealthy; they are not seeking unnecessary volatility or painful drawdowns. That is why we focus relentlessly on risk because in uncertain times protecting capital is just as important as growing it.

So, how high is up? That remains one of the great unknowns. What we do know is that discipline, diversification, and a clear focus on risk give us the best chance of navigating whatever comes next.

Over the course of 2025 we had the opportunity to read many thought-provoking books and have decided to highlight some of our favorites below:

The Art of Spending Money: Simple Choices for a Richer Life

By Morgan Housel. Writer and investor Morgan Housel, who we were pleased to host at our fall event in Toronto, offers a practical approach for managing wealth in ways that actually lead to greater happiness.

Die With Zero: Getting All You Can From Your Money And Your Life

By Bill Perkins. Billionaire hedge fund manager Bill Perkins offers a unique approach to wealth: spending and giving everything you have while you’re still breathing, in order to optimize for joy.

1929: Inside the Greatest Crash in Wall Street History – and How It Shattered a Nation

By Andrew Ross Sorkin. A narrative history by the CNBC host about the most devastating crash in history, with frightening warning signals that still ring today.

Principles For Dealing With The Changing World Order: Why Nations Succeed and Fail

By Ray Dalio. A timeless read by the hedge fund legend, documenting consistent themes throughout history among fallen empires.

Benjamin Franklin: An American Life By Walter Isaacson. The bestselling biographer offers a fascinating portrait of one of America’s founding fathers

Outlive

By Peter Attia. The former physician and researcher takes a dramatically different approach to managing health and longevity, focusing on increasing not only lifespan, but healthspan as well.

Year in Review 2025 – The Markets

Markets dealt with many cross currents in 2025. The first half of the year was dominated by trade concerns as the US raised tariff rates to levels not seen since the 1930s. Developed market equities fell sharply in early April but ultimately shrugged off the impact, while U.S. and China agreed to a one-year trade truce. In the second half of the year, risk-on sentiment drove an “everything rally,” and markets ended the year on a positive note.

Despite an uneven journey, 2025 was a solid year for equities. U.S. equities had a strong year with S&P 500 gaining 17.9% in U.S. dollar terms (12.4% in Canadian dollars) but were outshone by other regions.

Artificial Intelligence (AI) remained the dominant theme driving US equity markets, powered by continued investment in AI models, semiconductor demand, and the expansion of cloud and data-center infrastructure. The Information Technology sector significantly outperformed the broader market with returns of 24.6% over 2025. Communication Services followed closely at 23.1%. The two clear lagging sectors were Real Estate (2.6%) and Consumer Staples (1.5%).

For the first time in several years, non-US equities significantly outperformed the US market for the full year. A number of factors drove that break from U.S. exceptionalism, including a weaker U.S. dollar, geopolitical dynamics, attractive valuations outside the U.S., and a rotation by some investors away from US technology stocks.

The trade-weighted US dollar fell by 7.0% against a basket of global currencies, the steepest decline since 2009.

European markets outperformed the U.S. counterparts as well with the MSCI Europe Investable Market Index returning 28.7% (in Canadian dollars), propped up by strong returns from banks and defense stocks, and improving economic outlooks in Greece, Spain, and UK.

Emerging markets ended the year with a return of 27.3% (in Canadian dollars) by the MSCI Emerging Markets Index. The return was broad based with all regions posting positive returns, mainly driven by gains from the technology-oriented markets of Korea and Taiwan.

Bond markets also had a good year, with the U.S. Aggregate Bond Index gaining 7.3% (in USD). The defining narrative for fixed income markets in 2025 was the Fed’s resumption of a measured accommodative policy stance in the second half of the year.

The Federal Reserve (Fed) cut interest rates by 25 basis points in October and again in December, taking the federal funds rate to 3.5-3.75%. The Fed is navigating a delicate environment with rising unemployment and still-above-target inflation, keeping its dual mandate of stable prices and full employment in conflict. The recent decision to cut rates was not unanimous: some officials preferred to pause, while one advocated a larger cut, underscoring a divided FOMC.

The yield curve steepened, with yields falling in the shorter part of the curve, in response to the two rate cuts by Fed, while yields rose in longer maturities, reflecting investors’ concerns about the rising fiscal deficit.

Canada found itself navigating a markedly different path than anticipated at the start of 2025. Tariff uncertainties escalated globally, and immigration policy has been undergoing significant reform.

Yet amid these headwinds, the Canadian economy demonstrated resilience. The Canada-United States-Mexico Agreement (CUSMA) protections shielded most Canadian exports. Sector specific U.S. import tariffs have had a significant impact on some industries (auto and parts production, steel and aluminum among others), but an exemption from most tariffs for products compliant with CUSMA has kept most Canadian exports duty free – a key contributor to Canada’s resilience. CUSMA is due for renewal in 2026, which will bring some uncertainty and weigh on the economy.

The Bank of Canada cut the Overnight Target Rate by 25bps in its October meeting and held the key policy rate steady at 2.25% in its December meeting, citing positive economic data to support its decision.

On November 4th the Finance Department announced a new Federal budget, which committed billions in spending to help transform and strengthen Canada’s economy. In response to the planned spending increase, the budget will bring with it a larger-than-expected deficit.

Gold dominated the headlines as international central banks continued to diversify their reserve holdings, surging to its best year since 1979 (+66%).

In contrast to the precious metals, energy underperformed. Oil prices declined steadily through the year, with West Texas Intermediate crude ending 2025 at $57 USD per barrel. That represented a nearly 20% drop for the year, the sharpest annual decline in oil prices since 2020. The weakness reflected a combination of global oversupply, expanding production from producers, and softer demand growth amid slowing economic momentum.

As we turn the page to 2026, it’s important to keep the big picture in mind. Markets have delivered impressive returns over the past few years, but each year brings its own surprises. The market’s recent strong advance and the steep correction earlier last year are a good reminder that investing is a marathon, not a sprint. We can’t predict what lies ahead, but we believe a disciplined approach focused on long-term goals, diversification, and risk management is the best way to navigate the market.

Year in Review 2025 – Charts

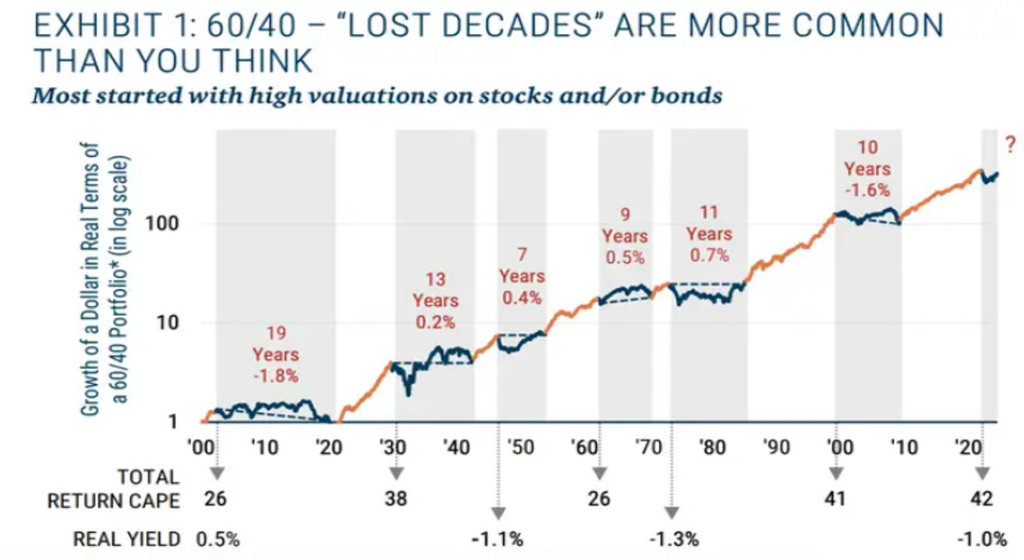

- The above chart shows six periods, averaging 11 years each, in which a 60/40 portfolio would have broken even or lost money.

- Those chapters have something in common – they all followed periods of exceptionally strong returns for the traditional portfolio.

- Today we are in a situation where equity markets have elevated valuations after a prolonged run of strong returns, a reversion toward longer term historical valuations would lead to disappointing medium-term results for a traditional 60/40 portfolio.

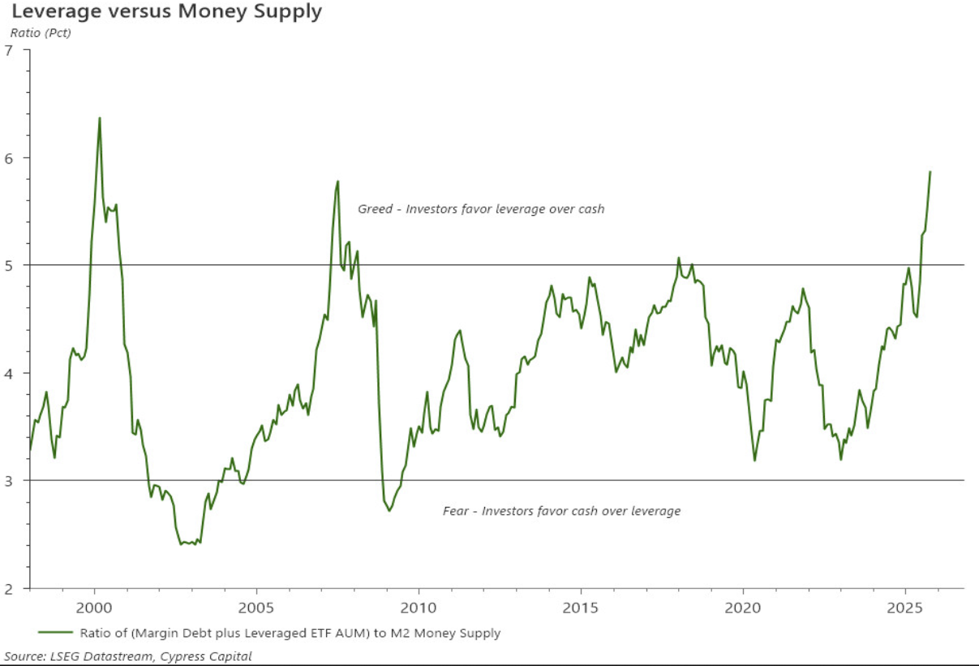

- The above chart shows the ratio of investor leverage (as measured by margin debt and funds invested in leveraged ETFs) to money supply (cash, bank accounts and money market funds).

- When the ratio is elevated (as it is today) it signals that investors are using more leverage relative to cash (i.e. taking on more risk).

- Currently the ratio is higher than at any other time except for early 2000 when the market was at the height of the dot-com-bubble.

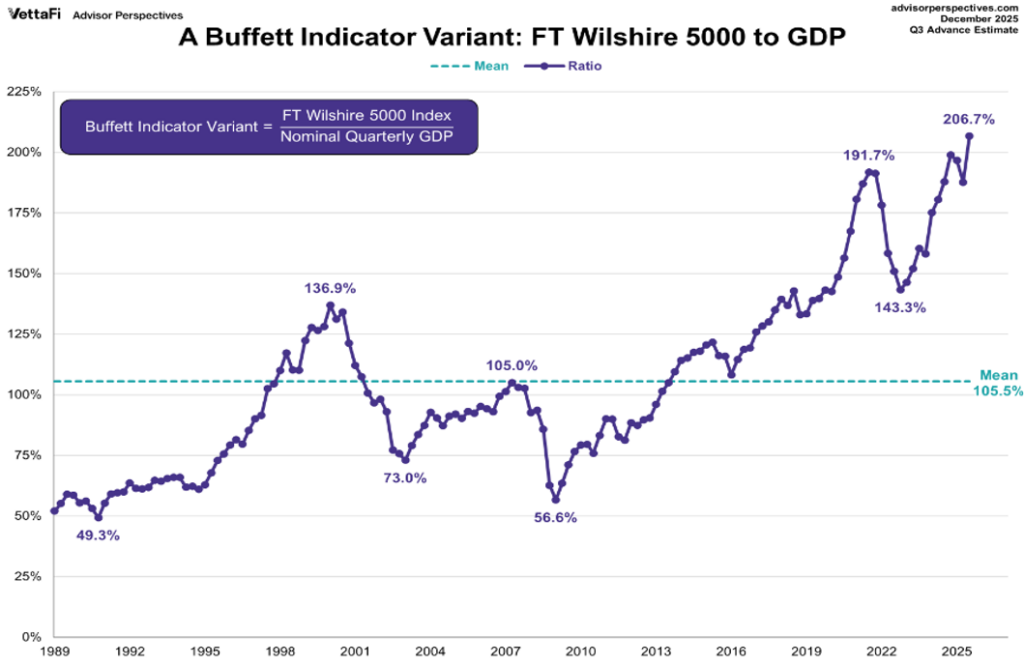

- The Wilshire 5000 Index, which is a broad-based stock index, divided by GDP illustrates stock valuations relative to the economy.

- This indicator of market valuation measures the market capitalization of public equities relative to Gross Domestic Product in the United States.

- When public market valuations are high relative to GDP (100%+), as they are now, that is an indication that markets may be overvalued.

Download a copy of this article in pdf here.

Insights

View AllNews & Events

News & Events

Keep up to date on Our Family Office's latest firm news, events, global and regional awards, as well as the latest announcements.

Tim Cestnick’s Globe & Mail Articles

Tim Cestnick's Globe & Mail Articles

Catch up on our Co-Founder and CEO, Tim Cestnick's weekly column. His status as an expert is reinforced by his role as a tax and personal finance columnist for The Globe and Mail, Canada’s most prominent national newspaper.

Investment Thinking

Investment Management

We provide tax-efficient preservation and growth of your investment assets, utilizing best-in-class global strategies, strategic asset allocation, rigorous due diligence on managers and their selection.

Podcasts

Podcasts

Our Family Office proudly presents the Our Family Office Podcast. Throughout the inaugural season, host Adam Fisch speaks to various experts from across our firm, offering insights into the areas of focus for an integrated family office, and the ways that a Shared Family Office™ can help Canada’s wealthiest families.